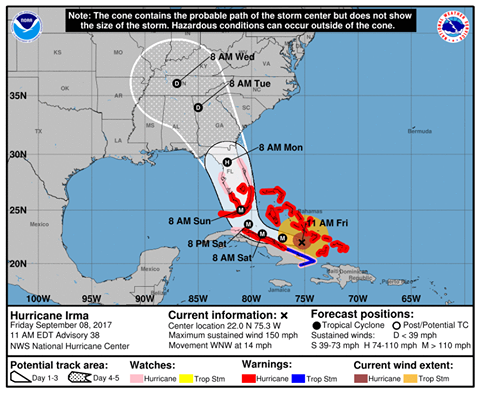

With Hurricane Irma continuing on a track that would bring its impact to all of Georgia, the state's insurance commissioner, Ralph Hudgens, is offering some advice that might help make recovery from any losses a bit easier, according to his office.

*Step One: Prepare For the Worst

· For personal safety, identify what storm shelter is available to you and prepare an evacuation plan. Choose two meeting places: one right outside your home in case of a sudden emergency, such as a fire; and one outside your neighborhood in case you can’t return home.

· Make a plan for your pets. Not all emergency shelters will take pets. Check with your local veterinarian for help with a plan.

· Take proactive steps to protect your property from loss. Install storm shutters or cover windows prior to a hurricane. Be sure there is no loose siding on your home and no damaged or diseased trees growing over your home.

*Step Two: Take an Inventory of Your Property

· It’s always a good idea to take photos or videos of your home before a disaster strikes to properly record the condition of the home. If you use a smartphone or digital camera, e-mail the photos to yourself, a friend or a relative or store them online.

· Take an inventory of your personal property, such as clothes, jewelry, furniture, computers and audio/video equipment. Photos and video of your home, as well as sales receipts and the model and serial numbers of items, will make filing a claim simpler. Leave a copy of your inventory with friends or relatives, e-mail it to yourself, and/or store it in a safe location. In addition, add insurance information to your inventory information — the name of your company and agent, policy number and contact information.

· Move all of your important documents to a safe location. Take them with you when you evacuate or store them in a safe deposit box outside the area.

*Step Three: Review Your Insurance Coverage

· Review your insurance coverage. What does your insurance policy cover? What does it exclude?

· The standard homeowners insurance policy does not cover flood damage. Check if your policy covers debris removal and sewer back-up.

· Find out if your policy covers additional living expenses to reimburse you for the cost of living in a temporary residence if you are unable to live in your home.

· If you have jewelry or collectibles, check the limits of coverage. You may want to buy more coverage for these items.

· What is your deductible? You will have to pay at least this much if you have a covered loss.

· Be sure you understand the difference between replacement cost and actual cash value. If your coverage is for replacement cost value and the cost to repair the property is greater than the cost to replace the property, the insurance company will reimburse you the dollar amount needed to replace damaged personal property or dwelling property with like kind and quality, limited by the maximum dollar amount listed on the declarations page of the policy. For example, if you own a five-year-old lawn mower that is destroyed by a fire, the company will reimburse you with an amount to purchase a new, similar lawn mower, minus your deductible.

· If your coverage is for actual cash value and the cost to repair the property is greater than the actual cash value of the property, the insurance company will reimburse you the dollar amount to replace the property minus the amount of accumulated depreciation. For example, if that same five-year-old mower was destroyed, and the average lawn mower lasts 10 years, the company will only reimburse you for half (10 years minus five years) the cost of the item, minus your deductible.

*Step Four: After Disaster Strikes and Your Home is Damaged

· File your claim as soon as possible. Call your insurance company or agent with your policy number and other relevant information. Your policy may require that you make the notification within a certain time frame.

· Be sure you cooperate fully with the insurance company. Ask what documents, forms and data you will need to file a claim. Keep a diary of all conversations with insurance companies, creditors or relief agencies.

· Be certain to give your insurance company all the information they need. Incorrect or incomplete information will only cause a delay in processing your claim.

· If your home is damaged to the extent that you can’t live there, ask your insurance company if you have coverage for additional living expenses.

· Take photographs/video of the damage.

· Make the repairs necessary to prevent further damage to your property (cover broken windows, leaking roofs and damaged walls). Don’t have permanent repairs made until your insurance company has inspected the property and you have reached an agreement on the cost of repairs. Be prepared to provide the claims adjuster with records of any improvements you made prior to the damage.

· Maintain any damaged personal property for the adjuster to inspect.

· Ask the adjuster for an itemized explanation of the claim settlement offer.

· Save all receipts, including those from the temporary repairs covered by your insurance policy.

· Be wary of contractors who demand upfront payment before work is initiated or payment in full before work is completed. If the contractor needs payment to buy supplies, go with the contractor and pay the supplier directly.

· Get more than one bid. Ask for at least three references. Check with the Better Business Bureau about the contractor. Ask for proof of necessary licenses, building permits, insurance, and bonding. Record the license plate number and driver’s license number of the contractor.

· If you can’t cover all of your expenses, contact your creditors to negotiate a payment plan.

· If there is a disagreement about a claim, ask the company for the specific language in the policy in question and determine why you and the company interpret your policy differently.

· If the first offer made by an insurance company does not meet your expectations, be prepared to negotiate to get a fair settlement.

· If you believe you have been treated unfairly in getting a claim paid, please contact us toll-free at 800-656-2298 or online at www.oci.ga.gov

http://accesswdun.com/article/2017/9/580097/hurricane-irma-georgia-insurance-commissioner-offers-advice-ahead-of-storm